Last week, digital media firm SVG Media Pvt. Ltd – which is a joint venture between Manish Vij’s Vun Network and Harish Bahl’s Smile Group – created a successful exit for its shareholders after being bought out by London-headquartered media agency Dentsu Aegis Network. Though the companies did not disclose the deal size, the transaction is pegged at nearly $130 million, making it one of the biggest acquisitions in the advertising technology space in India.

Founded in 2006, SVG Media -- which is operated by Smile Vun Group -- raised $3 million in external funding from Yahoo! Inc in its first year of operations. In 2011, Yahoo! sold its stake in the firm to US-based growth stage venture capital firm Xplorer Capital. The Gurgaon-based company – which competed with Google, Facebook and InMobi, among others – has generated almost 20 times returns to its shareholders, according to its founders. The acquisition marks the second successful exit for Vij and Bahl whose earlier venture Quasar Media was acquired by WPP in 2008.

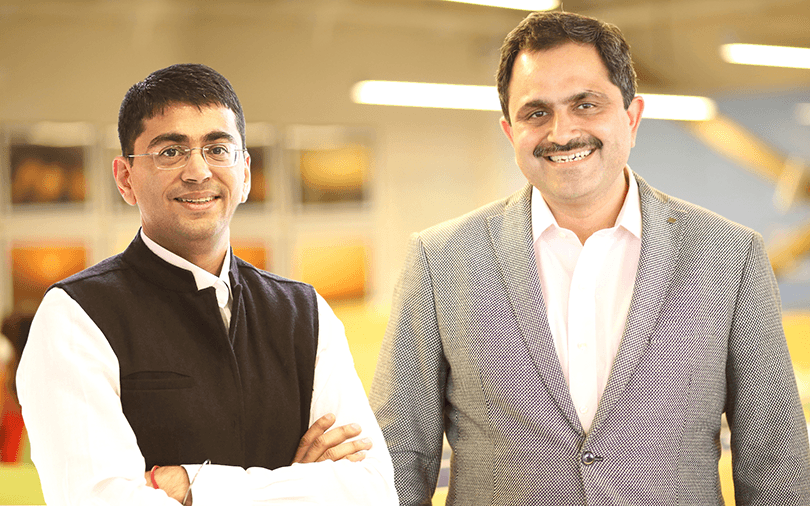

In an interview with VCCircle, Vij and Bahl talk about how SVG Media scaled up, digital media landscape in the country, rivals' valuations and why they chose acquisition instead of an IPO. Edited excerpts:

SVG Media was built at a time when most agency networks were apprehensive about digital advertising. Can you tell us how SVG Media evolved?

Vij: SVG is a continuation of our (Vij and Bahl's) partnership at Smile. The dot com buzz happened in 2000. In 2004, we started Quasar Media and in no time it became the largest digital media agency in India. However, even at that time, digital agencies were not seen as attractive and investors were not looking at that kind of businesses. When we were building Quasar, we realised that there was a need to form a technology-oriented digital media network because the user behaviour was changing and going a lot towards 'search'. We believed that there will be several digital media content companies but technology is required to consolidate the fragmented solutions. And, that's when the idea clicked. We then incubated SVG Media (earlier known as Tyroo Media Pvt. Ltd) from Quasar and started building it. When nobody believed in the ad-tech space, we did a lot of inorganic growth by acquiring businesses (such as DGM, Seventynine and Komli) and practically wiped out competition. We had to be either very small or very big to be profitable and we chose to be very big. Thus we acquired companies and built our business.

Bahl: We did things differently, and in hindsight, it was the right approach. When a lot of companies were chasing top-line and not looking at profitability, we chose the difficult path and thought that even if it takes a little longer, we will stick to generating profitability. Also, though SVG is a global business, we remained focused on becoming a strong market leader in India before we looked at any other market. That approach created a critical mass which gave us economy and scale. Besides, we followed a hybrid strategy of building and buying. We made Komli, DGM and NetworkPlay – which were not able to scale up – part of our group. We took the founders and key management people along and created an entrepreneurial culture and structure. That turned out to be the biggest differentiator because we were able to create a force of entrepreneurial founders hungry to achieve success and everyone played key roles in getting us where we were.

You were planning to take SVG public. What led you to scrap the IPO plan? Is acquisition only recourse for digital media companies?

Vij: Acquisition is not the only recourse. Though we have retained our technology business (Tyroo), we have postponed IPO plans for our newer businesses. We did work on doing an IPO but sometimes you have to make commercial decisions. We were weighing both strategic and IPO options and we decided that for investors and for the growth of the business, a strategic buyout looked to be a better option at this point of time. Having said that, in our entrepreneurial journey, we will certainly look at doing an IPO, for sure.

Bahl: The acquisition should be looked at positively. Our industry today lacks 'exits'. It would be easy to get 100 funding stories but difficult to get one successful exit. The digital advertising space is continuously changing; so we built two lines of businesses – one was technology-driven and the other was a service-oriented business. And, for the services business, we had to make sure the business was going into the right hands. The services industry globally and in India has always been better off with large marketing services groups. And, that is what we did with SVG Media by selling it to Dentsu. At a time when people were asking if India can create exits, the deal created a positive market sentiment.

InMobi is a unicorn. Last year, Mumbai-based Turakhia brothers sold off their ad-tech business Media.net for $900 million to Chinese companies. According to media reports, SVG got sold for $130 million. How do you view the valuation of your rivals?

Bahl: We followed an ‘India-first’ strategy. InMobi and Media.net are wrong examples to compare in terms of valuation because compared with their India business, SVG was a clear market leader. Looking at from a Smile Group perspective, we have a different strategy. SVG was just one business of the Smile Vun Group. Besides SVG Media, we have created value by building Quasar (75% of the company was sold to WPP in 2008); forming partnerships with Airbnb, Yahoo and others; setting up Africa-based digital agency SQUAD and scaling up technology business Tyroo. For us, the journey is still on. We look at each business separately. InMobi or Media.net were not even our competition as they targeted the global markets. We were way ahead of them in the Indian ad-tech space.

Vij: If you look at InMobi, it raised over $220 million in funding, including debt financing. From that perceptive, though it is a billion dollar company, it has generated four times returns on its raised capital. But we would have given about 20 times returns to our investors. So, our philosophy has been different on how we build businesses, market leadership and profitability without chasing funding. However, we are not out of the ad-tech game. We continue to build our business using Tyroo as our ad-tech vehicle.

What next?

Bahl: We do three things through one platform – investing in businesses, building businesses and doing joint ventures or partnerships with international firms that want to launch in emerging markets. SVG has been a great outcome. The capital will allow us to expand our focus on building businesses and tie-ups.

Currently, our focus would be on scaling up our businesses. We will be looking at increasing our global partnerships as we are seeing a lot of interest from global firms which are looking for Indian partners. We will announce some partnerships by the end of this month. Investing is another forte where we will keep supporting the entrepreneurial ecosystem and select founders with early-stage investments. Acquisition, too, will be part of our strategy.

Vij: Digital media spend is growing 30% year on year and digital will become second-largest medium after TV by FY2020 in the advertising industry. More importantly, television itself is becoming digital. There will be strong conversions and thus, it would be difficult to put TV and digital in two separate buckets after 2020.

Like this interview? Sign up for our daily newsletter to get our top reports.