A high-level advisory panel set up by capital market regulator SEBI last year has suggested major changes in norms to pool more domestic capital for private equity and venture capital funds besides creating a roadmap for securities transaction tax (STT)-based taxation for funds.

As first reported by VCCircle, the committee was set up early last year with Infosys co-founder NR Narayana Murthy as chairperson. Murthy, who stepped down from the board of the IT giant in 2014, had previously turned a private investor through his family office Catamaran.

The committee noted the rise in PE & VC deal activity in 2015 based on information attributed to VCCircle, using data from VCCEdge—the research platform of News Corp-owned VCCircle Network—and observed that domestic capital represents just 10-15 per cent of equity capital flowing into companies in India (be it startups or large firms) through PE and VC firms. Rest is foreign money.

In contrast, it added, in US and China, domestic sources fund 90 per cent and 50 per cent, respectively, of the venture capital and private equity needs of enterprises.

The 21-member committee that included several stalwarts of the industry including those representing KKR, TPG, Carlyle, IAN, TVS Capital and Piramal Group, called for several measures to boost domestic pool of capital for alternative investment funds (AIFs). AIF is a new classification of institutional investors representing, VC, PE and hedge funds under three sub categories. SEBI formed AIF norms four years ago.

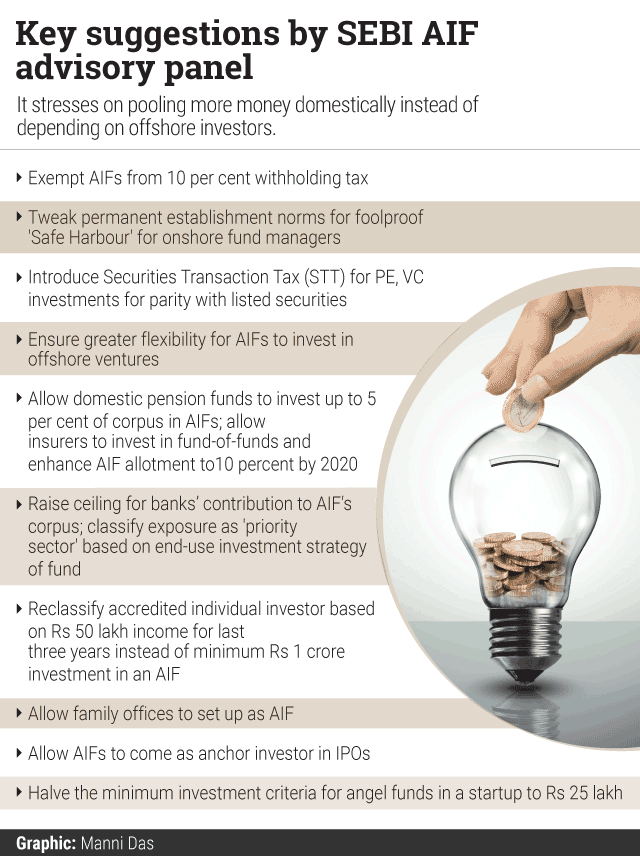

In particular, it called for channelling money from domestic pension funds including those managing the national employee provident fund, besides allowing banks and insurers to have a bigger exposure to PE, VC funds (see highlights box). If implemented, this could lead to a gush of capital flow to domestic PE, VC funds which currently depend on offshore investors.

Indeed, there has been a modest relaxation to allow insurers to invest in PE and VC funds already. The sector regulator IRDA permitted life insurance firms to put 3 per cent and general insurers to put up to 5 per cent of investible corpus in such funds in 2013. However, challenges remain. For instance, AIF investments are categorised as ‘unapproved investments’ requiring dual approval including the board of the insurance firm besides its investment committee. Besides, they are not allowed to invest in fund-of-funds (FOFs), or funds that then act as a master fund to other PE and VC funds.

The committee has called for easing these norms and hiking the ceiling of 3 per cent to 5 per cent of corpus for life insurers and thereafter for both types of insurance firms to 10 per cent.

It has also suggested allowing charitable and religious trusts to invest up to one-tenth of their money in AIFs. This is especially to pool in domestic endowment funds associated with top educational institutes such as IITs and IIMs. International university endowment funds are a big source of capital for PE and VC firms, including Indian funds that raise capital in the US.

The committee has said banks should be allowed to come as limited partner (LP or investor in PE, VC funds) with as much as 20 per cent of the overall fund size, twice the current amount. It has said this can be relaxed further to 25 per cent for social VC funds.

It has called for lower risk weight to banks’ investments in AIFs and said that if the investment objectives of such funds are consistent with the needs of the identified sectors, such investment should be treated as 'priority sector' investment and not impact the bank's capital market exposure. Banks currently have to meet certain minimum advances for such 'priority sector lending'.

In another key development, the committee said the regulation of who can invest in an AIF needs to be changed in line with international norms. Currently, an investor who wants to invest in such funds needs to shell out a minimum of Rs 1 crore. This is to keep out retail investors from betting on AIFs, considered risky and suitable for sophisticated investors.

The committee said this should be changed to allow any investor who has had an income of at least Rs 50 lakh for the past three years to pick units of such PE, VC funds. It said such people should be classified as accredited investors and they need not be registered with SEBI.

Another suggestion pertains to changing norms of limited liability partnerships (LLP) to allow them to have “investment†in the objects of business. This would be another enabler to allow more domestic capital to flow into AIFs.

It also asked for relaxation in norms to allow AIFs to participate in IPOs and family offices (private investment arms of entrepreneurs and industrialists) to be classified as institutional investors and indeed register as AIFs. Some of the more prominent family offices in the country include Wipro chief Azim Premji's PremjiInvest, Narayana Murthy's own Catamaran besides those representing Patni family (who sold Patni Computers) among many others.

The committee pointed for the need to relax norms for participation of NRIs in AIFs, allowing angel funds to invest in overseas ventures and halve the minimum investment amount in a startup by an angel fund to Rs 25 lakh to channel money to more startups.

It has also called for relaxing the upper limit on the number of investors who can participate in an angel fund from 50 to up to 200. For more on specific suggestions related to angel investments and startups, click here.

Taxation

The draft report also talks at length about taxation reforms to boost the AIF industry at large. In particular, it asks for more efficient tax pass-through framework by exempting income of AIFs from withholding tax and their investment gains to be deemed ‘capital gains’. It also talks about allowing set-off of losses incurred by AIFs to their investors.

It said overseas investors in India-centric fund vehicles should not be subject to the indirect transfer provisions of the IT Act when they transfer their investments in an India-centric vehicle to another investor.

In a critical suggestion, the committee also asked for making 'safe-harbour' more effective for managing funds from India. Currently most fund managers of offshore funds manage their investments from locations overseas rather than from India.

“In order to attract significant amounts of foreign capital by having fund managers based in India, it is important that their operations in India are not treated as permanent establishments under DTAAs,†it said.

The report noted that the existing safe-harbour provision of the government is not effective for onshore India-based managers of offshore private equity and venture capital funds. It recommended changes related to: investor diversification, control or management of portfolio companies, tax residence, arm’s length remuneration of fund managers and annual reporting requirements.

Another key suggestion by the committee pertains to introducing securities transaction tax (STT) for private equity and venture capital investments, including SEBI-registered AIFs to bring parity with the taxation of investments in listed securities.

“Given the high risk and relatively illiquid and stable nature of private equity and venture capital, it needs to at least be treated at par with volatile, short-term public market investments for taxation,†the committee noted.

It has said that the government should adopt a roadmap for AIF taxation based on the STT framework and after that income from AIFs should be tax free to investors.

Besides PE and VC industry heavyweights, it also had representation from finance ministry, RBI, SEBI, consultancies and other financial services firms.

SEBI has asked for public feedback on the proposals by February 10. For full report .