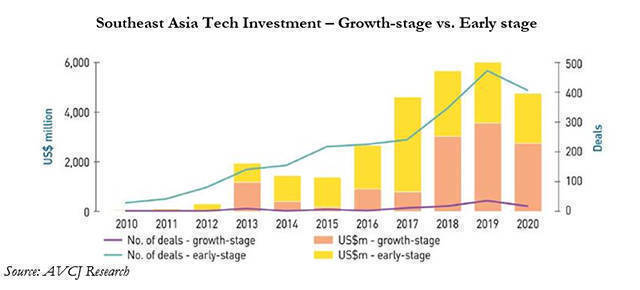

The year 2018 marked a shift in the Southeast Asia technology sector, as the volume of growth-stage private equity investments surpassed early-stage investments for the first time. Private equity investors have been attracted to the scalability potential of the region’s internet economy, expected to triple from its 2019 level to US$ 300 billion by 2025 on the back of secular trends such as democratization of the internet, transition to a digital economy and the globalization of innovation.

The Covid-19 pandemic has acted as a catalyst to these changes, by compressing three years of changes into one year, and in particular by fast tracking monetization as consumer behaviour evolves from simply “using the Internet for free” to “transacting and paying for products and services on the Internet”.

As these forces have combined to reconfigure the typical risk profile of a technology start-up investment, the private equity industry has moved into late-stage technology deals that were once solely confined to the realm of venture capital investors. The potential for alpha capture in the fast-growing tech universe, along with the diversification opportunity it provides, has attracted demand across the global PE landscape. In the US, annual private equity investment in venture capital deals grew more than sixfold from 2010 to 2019. In 2020, PE firms have participated in over 800 VC transactions worth a combined US$ 48.3 billion with an average transaction size of US$ 60 million, both all-time high figures, as per data released by Pitchbook.

Within the PE landscape, growth-stage private equity is the most perfectly suited asset class to capitalize on this shift. Placed at the intersection of private equity and venture capital, growth stage PE firms typically invest in transactions in the range of US$ 10 - 100 million, backing companies with proven unit economics and working with management to drive value add through operational improvements and revenue growth. As technology start-ups mature towards a proven model of repeatable and scalable customer acquisition in established markets, they increasingly fit the growth equity playbook for profitable revenue growth, with risks centred around execution and scalability.

Nowhere is this trend more evident than in India, where favourable demand side along with supply side dynamics have led to a growing maturity in the start-up ecosystem. The Reliance Jio led mobile revolution, which has brought about a 95% decline in data costs since 2013, has resulted in one of the world’s largest mobile user bases of 450 million consuming an average monthly of 11GB (2019). This large and growing user base has, in turn, provided the fertile substrate for the e-commerce growth that India has witnessed — having grown at a CAGR of 30%+ over the past three years, reaching a critical size US$ 30 billion in FY20.

With the onset of the Covid-19 pandemic, online purchases increased 30-50% across categories, with Tier 2 cities demonstrating the same level of digital adoption as Tier 1 cities. It is expected that the majority of this accelerated demand will be retained, and the total e-commerce market is forecast to grow by nearly 4x in the next five years, reaching US$ 118 billion in FY25. The broader monetization opportunity of the N2B (next two billion people embracing digital across India and ASEAN) is expected to open up a total addressable market in the range of US$ 800 billion -1.1 trillion, with revenue opportunity in the range of US$ 70-145 billion by 2025.

On the supply side, India is also home to a thriving ecosystem of over 3 million software developers. This engineering talent, developed over nearly 3 decades by its IT industry, is one of the largest globally with revenue of US$ 190.5 billion as of FY20. English speaking, offering a wide variety of technical skills and capabilities and still affordable, India’s skilled IT workforce comes with a significant wage arbitrage factor, resulting in cost savings in the range of 15-20%. These factors, combined with the inherently frugal nature of India’s technology start-ups, has enabled start-ups to keep a healthy margin profile as they scale.

The combination of scalability and margin improvement is enabling the emergence of credible start-ups with domain expertise that have the ability to become category leaders in specific segments in India and the ability to serve global markets from India, hence creating attractive opportunities for PE firms. For instance, within the segment of SaaS alone, this maturity is evidenced by a more than 2X increase in the average deal value of a SaaS investment in India over the past five years, which reached nearly US$ 50 million by 2020.

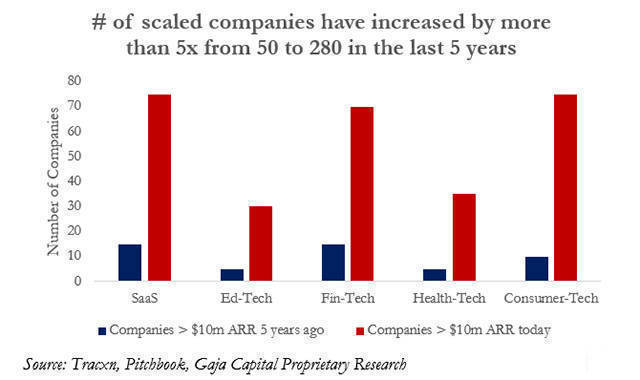

Gaja Capital believes that this combination of scalability and margin improvement has reconfigured the risk profile of technology, from what was a venture capital investment into an attractive opportunity for growth stage private equity. There is now a growing number of companies that exceed US$10 million in ARR today across ed-tech, fin-tech, health-tech, consumer tech and SaaS, in India. Our recent investments in Xpressbees (a leading ecommerce-oriented logistics player) and Leadsquared (a leading sales tech CRM company) are examples of this trend. With the venture capital ecosystem delivering on the “Zero to One” and the “One to Ten million dollars in scale”, there is now a growing opportunity for growth stage private equity investors to work closely with these companies and help them scale to US$ 100 million and beyond. GPs with active engagement models, operational value-add capability and ability to work closely with such companies in helping them scale profitably, will be the winners in this transition.

Brand Solutions is a marketing initiative for sponsored posts. No VCCircle journalist was involved in the creation of this content.