Analysts, investors and journalists who follow stocks have an obsessive focus on earnings per share, what it is now and what it will be in the future, as can be seen in the earnings announcement game every that takes up so much of Wall Street’s time and resources. Not surprisingly, acquiring firms, considering new deals, put their accountants to work on what they believe is a central question, “Will the earnings per share for the company (acquirer) go up or down after the acquisition?†A deal that will result in higher earnings per share, post-deal, is classified as accretive, whereas one that will cause a drop in earnings per share is viewed as dilutive.

Is it better to have an accretive or a dilutive deal? If you asked that question of most investors, analysts or even CFOs, the answer, you would be told, is obvious. An accretive deal is better than a dilutive deal, with the logical follow through that if your earnings per share increase, your stock price will follow. But is that true? To see why it is not, let us break down the mechanics of what will happen to earnings per share, after an acquisition or merger. The net income of the two firms will be cumulated and divided by the number of shares outstanding in the combined firm, after the merger. Mathematically, here are the two factors that will determine whether a deal is accretive or dilutive:

1. What are the relative PE ratios of the acquiring/target firms? In a share swap, where the acquiring firm’s shares are swapped for the target firm shares, the combined company’s earnings per share will increase (be accretive) only if the PE ratio of the acquiring firm is greater than the PE ratio for the target firm. It will be dilutive, if the reverse is true.

2. How will the deal be financed? If a deal is funded with cash on hand or by issuing new debt, the deal will be accretive, if the company being acquired is profitable and is generating a high enough expected income to cover the lost interest income (if cash is used) or the expected interest expenses (if debt is used).

If you are interested, you can download a simple spreadsheet that works out whether a deal will be accretive or dilutive to the acquiring company.

Reviewing these two conditions make it clear why it is absurd to think that accretive deals are always good and that dilutive deals are bad. The Achilles heel in this reasoning is in the assumption that the PE ratio will stay fixed after the deal; if that were true, higher EPS will always translate into higher price, making accretive deals good for acquiring company stockholders. But it is not, and you can see the rationale by looking at all of the scenarios listed above:

1. If you are buying a company with a lower PE ratio than yours, there is usually a good reason why that company has the lower PE. It could be that the firm is riskier than average, has lower or no growth or is in a business with sub-standard returns. If any or all of these reasons hold, acquiring this company will bring those problems into the combined company and cause the PE ratio for the combined company to fall. If that drop exceeds the increase in EPS, the stock price of the combined company will also fall, notwithstanding the accretive nature of the deal.

2. If you are funding a deal with cash, the deal will almost always be accretive because the income you are generating from cash (especially at today’s low interest rates) will generally be lower than the equity earnings you will get from the company that you are acquiring. But is that value enhancing? Not really. Replacing an investment that generates 1% riskless today with a risky investment that generates a 4% return will make investors in the company worse off, not better.

3. If you are financing the deal with debt, the deal will be accretive if the equity earnings that you generate from the acquired company exceeds the interest expense. But here again, that is not a sufficient condition for value creation. You are contractually committed to make the interest expense, while the income you anticipate is “riskyâ€. The basic tenets of the risk/reward trade off will require a much higher risky equity return than the interest rate on the debt you take on for the deal to be value creating.

Using the same type of reasoning, you can see that it is possible for a dilutive deal to be value creating: the target firm may have higher growth/higher quality growth/lower risk than you do and acquiring it may push up the combined firm’s PE and/or there may be enough growth in the firm that even though the current earnings don’t cover your interest expenses/foregone interest income, the future earnings will comfortably. It is therefore entirely possible for an accretive deal to be value destroying and a dilutive deal to be value increasing.

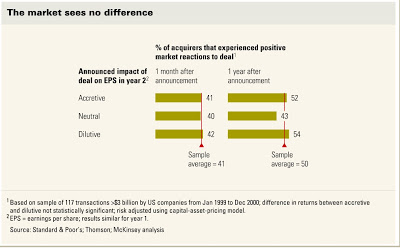

There are CFOs who will hear this argument and say that it is “academicâ€. The market (and the equity research community) care about earnings per share, they will argue, and it is not sophisticated enough to make the adjustments to PE for risk and fundamentals. The proof, though, is not in what CFOs believe or what equity research analysts say matters, but in how the market reacts to accretive and dilutive deals. A McKinsey study of accretive and dilutive deals uncovered the following market reactions to these deals:

Note that at least in this short sample period, there is no evidence that markets reward accretive deals and punish dilutive deals. Thus, Leo Apotheker’s defense, offered two days after HP bought Autonomy, that “Autonomy will be, on Day 1, accretive to HP†would have rung hollow, even without the benefit of hindsight. I, for one, think that it is time that we consigned this dilutive/accretive analysis to where it belongs: the dustbin. It is not only truly useless in assessing the quality of deals, but worse, it allows companies to justify (at least to themselves) some really bad deals.

Posts on acquisitions

Acquisition Accounting I: Accretive (Dilutive) Deals can be bad (good) deals

(Aswath Damodaran is a professor of finance at the Stern School of Business at NYU.)