“The secret of long-term investment success is benign neglect. Don’t try too hard. Much success can be attributed to inactivity.†- Warren Buffett

Most investors today are obsessed with momentum investing that at times many good businesses lying at low valuations often get neglected – the realisation comes only after the stock prices of such companies have gone up a few times.

We at Hidden Gems have always believed that one of the fastest ways to make money and sustainably beat the markets is by tapping an under-mined business niche; and get in before the large investors do.

We look at 3 companies in niche business which could be wealth creators in the coming years.

Zicom Electronics – a company involved in Electronic Security products which and a Numero Uno in its business segment and with good business potential, going at a market cap of Rs.150 crore ($36 mn) ;

Venky’s India – a company driven by India’s consumption boom and the leader in the poultry segment; paid tax of Rs.15 crore and generated cash profit of Rs.35 crore and with uninterrupted dividend track record of over 18 years, going for a market cap of a mere Rs.120 crore ($29 mn)

Selan Exploration – an oil exploration company generating cash profit of Rs.25 crore for a quarter (Apr-June 08) and having high operating margins (over 85% in Apr-June 08 quarter). Interestingly, the most of the company's oil assets are yet to be mined and with the recent success in the recently concluded drilling program, we view the company with a renewed optimism. The company is available at Rs.400 crore market cap. ($95 mn)

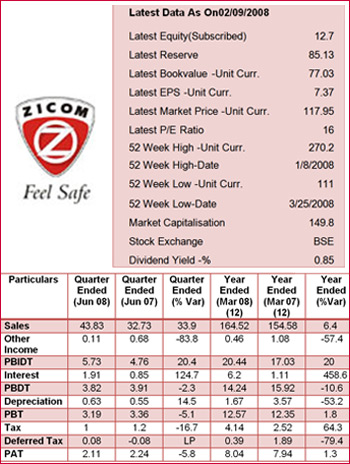

Zicom Electronic Security Systems Ltd. (Current Market Price Rs.118)

Zicom Electronic Security Systems Ltd. (Current Market Price Rs.118)

The rising burglaries and armed robberies have hightened the need for electronic security surveillance, an area neglected in the past.

Zicom Electronics, a company operating in the Electronic Security space has created a niche for itself in the electronic security market space with offerings for both the home and institutional segment. The company today is the leading electronic security solutions provider in the country, with offices in over 50 cities and towns. The company offers a wide range of products including access control Systems, CCTV surveillance, fire alarm systems, smart cards, biometrics, remote video surveillance, perimeter protection system, law enforcement products, etc.

The company has also integrated all this multiple security applications into one coordinated hardware and software package.

The company provides Electronic Security Surveillance solutions to British Airways, Siddhi Vinayak Temple, RBI, Star TV, Reliance, Tetrapak, Taj Hotels, Haji Ali Dargah, Mumbai Traffic Police, Prince of Wales Museum, NTPC and BARC, to name a few.

Zicom has a tie-up with Future Media which allows it to have exclusive retail outlets at over 100 outlets of Future Groups select retail formats including Big Bazaar, Brand Factory, E-Zone, Electronics Bazaar etc. Besides, the company has an ambitious rollout plan of exclusive Zicom Retail stores and has targeted 300 stores by 2009.

It has also made several investments in subsidiaries :-

--The company has acquired 49% stake in Unisafe Fire Protection Specialists L.L.C, Dubai in UAE. With this acquisition, the company aims to gain a foothold in the infrastructure growth in the Middle East and West Asian markets.

--The company has set up a subsidiary in Hong Kong for taking up manufacturing activities in China and to promote international sale of Zicom branded products.

--The company has entered into a Joint Venture with Singapore based CNA Group to offer high end intelligent building management solutions and green buildings. Zicom will hold 51% and CNA Group 49% in the JV company Zicom CNA Automation Ltd.

Security is a business which has got an enormous potential in India – be it Commercial Buildings, Offices, Homes, Malls, Supermarkets, City roads, Airports, Railway stations, - Electronic Security surveillance would become essential in the coming times. Imagine the Traffic Cop sitting in the Central Control Room controlling traffic with the help of the Electronic Eye rather than standing on the city roads.

Zicom's business model allows it not just one time sales revenues but recurring service revenues year on year.

The concept of Electronic Security is still in its infancy as far as India is concerned – the growth of middle class, improving lifestyles, concern for Home Security with rising crime graph coupled with falling hardware prices makes a perfect case for demand explosion in the sector. Of late, we are witnessing the old favourite DING-DONG Bell in our homes getting replaced by Video Door Phones. Moreover, the ongoing real estate boom has put the company in a sweet spot with increased order flow being witnessed. The company has already received contracts from various builders for its home security products like Burglar Alarm, Electronic Gas Leak sensor and Video Door Phones.

The Indian security Market is dominated by companies like Zicom, Honeywell, Tyco, Johnsons Control and Godrej, while the Home and Retail segments are dominated largely by unorganized regional players where the focus is standalone products and not solutions - Zicom probably being the only organized national player. The company is scouting for buys in US and UK which will enable it to have a global footprint in the Electronic Security market.

Our major concern however is low promoter’s holding in the company (17.84% as on June 30, 2008) – this may however act as a double edged sword. On one hand, low promoters holding leaves excessive float in the market, on the other hand, makes the company susceptible to being preyed upon by potential raiders. Inspite of the concern, we believe that space in which the company operates, the potential is high. The company’s market cap is a mere Rs.150 crore at the current price of Rs.120.

Venky’s India Ltd. (CMP: Rs.124)

Think chicken and the first name which comes to mind is Venky’s.

Think chicken and the first name which comes to mind is Venky’s.

Venkys India Ltd. is a leading producer of poultry products in India. The company’s product portfolio includes animal health products, pellet feeds, processed, and further processed chicken products, solvent oil extraction, and Specific Pathogen Free Eggs.

The Venkateshwara Hatcheries Group also caters to the related requirements of the poultry sector, such as poultry feed, vaccines, medicines and health products. The Poultry & Poultry Products business accounts for lion’s share of the revenues of the company. The other major contributors to revenue include Poultry Feed, Animal Health Products, and Solvent Extraction. Diversifying from mainstream poultry products, Venkys (India) Limited has added to its credit, manufacturing facilities for nutritional health products for humans, and pet food and health care products. The company has steadily grown to over 30 units spread across India.

The company also produces high-tech specific pathogen-free eggs (SPFE). The company's Specific Pathogen Free Egg unit is among four such units in the world and the only one of its kind in the developing world. These eggs are used for making vaccines for human beings and chicken as well. Though this business accounts for only 6% of total revenues, its profitability is very high. The company produces a wide range of animal health products like antibiotics, growth promoters and feed supplements.

We like the business model of the company – the company has presence in both the Institutional and Retail segment. Venky’s is a national brand and enjoys the positioning of a hygienic premium product and has a nationwide distribution network. The company faces competition from the unorganized sector in the Processed Chicken segment. However, the company has carved a niche for itself and supplies its products to quality-conscious institutional consumers in the hospitality industry. These include Domino's, KFC, Mc Donalds and Pizza Hut, major five star hotels and flight kitchens. The company is witnessing a good growth in demand from this segment. The company also sells various poultry products in the ready-to-eat segment through a nationwide distribution network. These products are sold under the brand name VENKY’S and are available at Supermarkets and retail stores in all major cities in India.

Taking a stake in Venky’s India is akin to taking an exposure in the Indian Poultry industry, at a ridiculously low market cap of under Rs.120 crores. The stock is currently underowned by the Institutional Investor. However, given the size and scale of operations of the company and its leadership position in the Industry, the stock has the potential to attract the Institutional Investors.

Our major concern is a host of other promoter controlled companies involved in the same business, which could lead to a conflict of interest with the public listed company. Other concerns being outbreak of Bird Flu and rise in Maize prices, which can adversely effect profitability.

The market cap of this leader of the poultry industry at its current price of Rs.125 is Rs.120 crores. This for a business which paid a Tax of Rs.15 crores, generated a Cash Profit of Rs.35 crores (for FY 07-08) and has a track record of uninterrupted dividends for last 18 years.

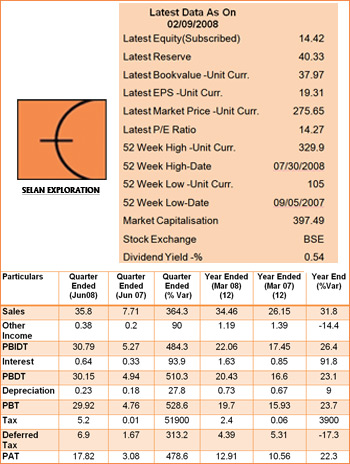

Selan Explorations Technology Ltd. (CMP: Rs.275)

With high crude prices and limited resources, companies in the Oil Exploration business could be potential winners. Selan Exploration with proven blocks and with 100% ownership of all the five blocks could be an Outperformer.

With high crude prices and limited resources, companies in the Oil Exploration business could be potential winners. Selan Exploration with proven blocks and with 100% ownership of all the five blocks could be an Outperformer.

The year 2008 could be inflexion point for Selan Exploration for its business to mature to a level of fast growth. To give a brief background, the company was awarded the BAKROL, INDRORA and LOHAR oilfields in Gujarat for development in the year 1993. These fields are located in Cambay basin in Gujarat. Cambay Basin is an oil rich region and has been categorized as Category I sedimentary basin meaning commercially productive region. In the year 1997, the Company received Letters of Intent for two additional fields in onshore Gujarat viz KARJISAN, a gas field and OGNAJ, an oil field, from the Ministry of Petroleum and Natural Gas (MoPNG). Thus, in all the company has been allotted 5 Oil/ Gas fields.

Business Model – Relatively De-risked - Unlike other Oil Exploration companies, Selan Exploration has invested in Exploratory blocks that have a track record of proven commercial production. This benefits the company in two ways – one the company doesnot have to invest in the exploratory activities which could consume time and money and two, it means that company is not exposed to the inherent risk associated with the exploration business.

Major portion of the current production of the company comes from the BAKROL filed. During the financial year 2007-08 the Company produced 1,20,000 barrels of crude oil. This production came from a total of 14-15 Oil wells.

The first quarter numbers of the company (Qtr Apr-June 08) came out as a pleasant surprise, wherein the Sales shot up 365% to Rs.36 crores and PAT shot up 478% to Rs.17.82 crores. Operating Profit was Rs.30.79 crores – OPM of over 85%. Let us see how the company has achieved this and why I am calling this as the inflexion point for the company.

First, let us analyse how the company managed such huge increase in Sales and Profitability – this was on account of two factors – higher Crude Price and substantial increase in production. The company realized an average of US$ 116 per barrel for the quarter Apr-June 08 as against US $ 76 per barrel for FY 07-08. The company undertook a Capital Expenditure programme in Jan-Mar 08 for Rs.30 crores.

The company drilled 7 more wells under the capital expenditure programme, out of which one will probably not produce (management has not given up yet on the 7th one). In the quarter Apr-June 08, the company produced 72,000 barrels as against roughly 30,000 for the corresponding quarter last year. We wondered how there was an increase of 140% in production whereas the increase in the number of wells is less than 50% - obviously the new wells were producing at much higher rates. The management attributes this to a different technology which they employed this time which has resulted in the flow from the new wells being more than double compared to old wells.

If you analyze the first quarter numbers more closely, the PAT of Rs.17.82 crores has been derived after providing for a Deferred Tax Liability of roughly Rs.7 crores making the Cash Profits as Rs.25 crores. If you check up the past history of the company, the management has been conservative and has used Internal Accruals and small debt for carrying out Capex. Now, with Cash Profits of roughly Rs.25 crores in a quarter, the company can witness sustained exponential growth in the coming years.

Not to forget - the company is currently concentrating only on BAKROL Oil Field at the moment (where the reserves have been revalued at 73 million barrels as against 43 million barrels earlier). The other 4 fields are still virgin with a lot to be done. Certainly good times seem to have just started for the shareholders of Selan.

(Ashish Chugh is an equity analyst and investment consultant based at New Delhi. At the time of writing this article, he, his firm and dependent family members have a position in the stocks mentioned above. The author, his firm or any of his dependent family members may make purchases or sale of the securities mentioned in the report while the report is in circulation. The author invites readers to send him email and welcomes comments, feedback & queries at nexgenfin@yahoo.com.

This report has been prepared solely for information purposes and the information contained herein may not be deemed to be an investment advice. Such information is impersonal and not tailored to the investment needs of any specific person. The information contained herein is not a complete analysis of every material fact representing any company, industry or security. The views expressed may change. While the information contained herein has been obtained from sources believed to be reliable, no responsibility (or liability) is accepted for the accuracy of its contents. Investors are advised to satisfy themselves before making any investments and should consult with and rely upon their own advisors whether and how to use such information in making any investment decision. Neither the author nor his firm accepts any liability arising out of use of the above information/ article.)