Over the last few years, asset management in India has witnessed significant traction with the capital markets regulator Securities and Exchange Board of India (SEBI) promulgating reforms to the regulations governing privately pooled investment funds, portfolio managers and investment advisers.

Interestingly, what began in its nascent stage as an interventionist regulatory framework intended to ensure investor protection, now seems to be moving towards a caveat emptor or ‘buyer beware’ regime, relying on the well-informed decision-making of sophisticated, big ticket investors with higher risk appetite.

The principle of caveat emptor is enshrined in SEBI’s recent introduction of the concept of accredited investors (ACIs) across its regulatory regimes governing investment funds, portfolio managers and investment advisers.

The concept of ACIs is well-established in evolved asset management jurisdictions such as Singapore, Hong Kong and the United States of America, for whom certain regulatory requirements are relaxed in consideration of their higher risk appetite and possession of industry specific knowledge.

While close regulatory oversight has been a defining characteristic of SEBI regulations in the past, the introduction of ACIs is a welcome step, in line with the long-standing industry ask of differentiating between retail and sophisticated investors.

In this update, we analyse recent Gazette notifications dated August 3, 2021 amending the SEBI (Alternative Investment Funds) Regulations, 2012 (AIF Regulations), the SEBI (Investment Advisers) Regulations, 2013 (IA Regulations) and the SEBI (Portfolio Managers) Regulations, 2020 (PM Regulations) (collectively, the Amendments) which have introduced the concept of ACIs across the three regulations.

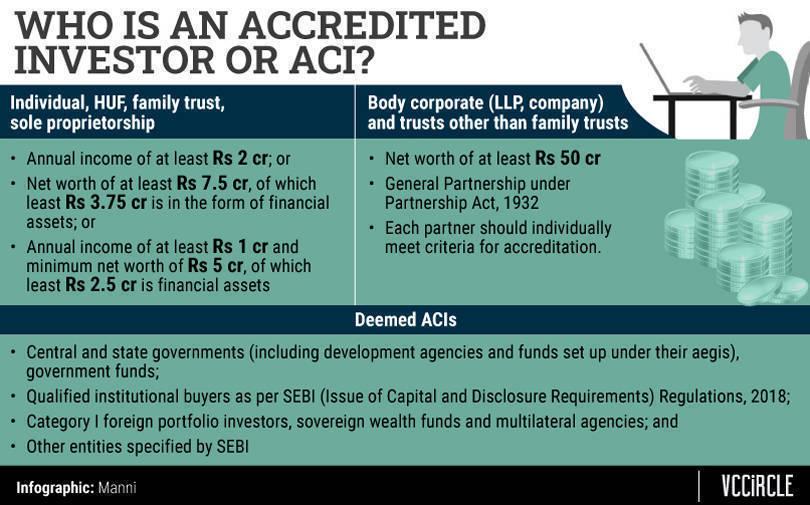

Who is an ACI?

In February 2021, SEBI released a consultation paper outlining the construct of ACIs seeking public comments (consultation paper). The culminating amendments to the AIF Regulations provide a broad definition of ACIs, summarised below, subject to their due certification by an accreditation agency (being a subsidiary of a recognised stock exchange or depository or other entities as may be specified by SEBI):

IA Regulations have also adopted the above construct of ACIs (as enshrined under AIF Regulations). However, a slightly modified approach has been adopted for the purposes of the PM Regulations, which define ACIs as persons fulfiling the eligibility criteria as prescribed by SEBI and who have been granted a certificate of accreditation by an accreditation agency.

We expect that SEBI will soon issue circulars detailing the conditions governing accreditation agencies and the grant of certification to ACIs for each of the aforesaid regulations.

Specific relaxations for AIFs, PM and IA

The amendments make the following changes to the regulatory regime:

AIFs

The amendment to AIF Regulations introduces the concept of large value funds for accredited investors (LVFAIs), which are AIFs raising money only from ACIs (except commitments from their manager, sponsor or the manager’s employees or directors), each of which commits a minimum of Rs 70 crore to the fund.

LVFAIs will benefit from relaxed diversification norms – permitting Category I and II AIFs to invest up to 50% of their investable corpus in a single portfolio company (as compared to the 25% limit for other AIFs of the same category) and Category III AIFs to invest up to 20% of their investable funds (as compared to the 10% limit for other AIFs of the same category). This enables LVFAIs to explore deals with double the ticket size that is otherwise permitted for other AIFs of the same category.

Additional dispensations available to LVFAIs include the ability to extend their tenure beyond the two-year limit as per their fund documents. AIFs facing end of their tenure face typical challenges due to stringent timelines of AIF Regulations, and are required to enter the liquidation stage after exhausting the two-year extension permitted under the AIF Regulations, even where commercially the investors and the manager do not deem it as the best option for the fund.

Failure to do so may be viewed as contravention of the AIF Regulations. LVFAIs, however, may now extend their tenure as per their fund documents providing higher flexibility in charting the fund’s own course.

LVFAIs are also exempted from the requirement of filing the private placement memoranda of their subsequent schemes with the SEBI thirty days prior to the launch of a scheme, easing regulatory vetting once the AIF registration has been granted.

As per the existing SEBI norms, LVFAI will also benefit from exemption from the PPM format prescribed by SEBI and can procure waiver from the liability prescribed for AIF’s investment committee, subject to certain conditions.

Portfolio management

Drawing on amendments to the AIF Regulations, the PM Regulations have now introduced the following concepts:

- Large value accredited investors (LVAIs) that invest at least Rs 10 crore with the portfolio manager: The requirement to enter into an agreement for rendering services to such investors in the format prescribed with SEBI has been dispensed with for LVAIs.

Further, a portfolio manager may provide services for investments in unlisted securities for up to 100% of the assets under management of an LVAI, subject to adequate disclosures and contractual agreement; and

Investment advisory

The consultation paper contemplated providing exemption to IAs working with ACIs from the requirement of incorporating the mandatory terms of the client-IA agreement and from the limits and modes of fees charged by IA.

While the amendments have merely recognised the concept of ACIs for the purposes of the IA Regulations without providing any specific benefits, it is expected that the benefits mooted under the consultation paper will soon be notified by SEBI.

Global comparison and way forward

A cursory look at the regulatory regime in a few evolved and mature asset management jurisdictions (such as Singapore and United States of America) reveals one commonality – that the governance of an investment fund or an advisory platform is generally governed by the terms of the contractual arrangement between an investor and the advisor.

Needless to state, if India has to compete with its counterparts in terms of providing a robust and conducive environment for asset management, it should provide adequate leeway to accredited investors in negotiating the terms of their engagement with their professional advisors. For this reason, freedom from regulatorily prescribed formats, agreements and documentation is a welcome step.

Specifically for LVFAIs, a case for exempting them from the conditions prescribed by SEBI for undertaking leverage and borrowing by AIFs, and from the restrictions on issuing units to specific investors with segregated portfolios also seems justified.

In our view, the amendments are a fresh change of direction in the regulators’ approach towards regulating Indian asset management and advisors.

Vivaik Sharma is a partner and Rohan Priyadarshi and Swaha Sinha are associates at Cyril Amarchand Mangaldas. Views are personal.