With sellside economists’ GDP estimates being cut regularly (our estimate remains above 7%), with the INR in a free (our target INR/US$56-58), India's star appears to be fading. However, as shown by a series of long term charts in this note, the Indian market is unquestionably ‘cheap’ now. Whilst given the scale of the European crisis and given India's comatose Government, it is easy to be bearish on India, these charts suggest that now is almost as good a time as any to BUY India. The country will rarely look as attractive on valuations when the world economy perks up and when India's growth hits its cyclical peak (v/s the cyclical trough that it is

at now).

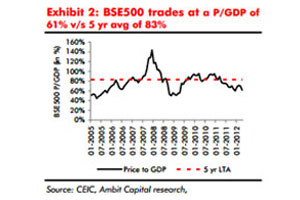

India appears oversold on long-term metrics

India appears significantly oversold on a comprehensive set of relative valuation metrics based on book value, national income and cyclically adjusted earnings

(refer to the right hand margin). In fact, India has appeared cheaper than it is at present only once or twice in the last ten years:

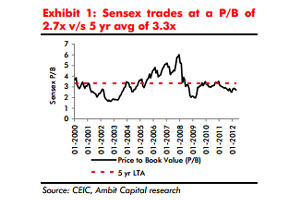

P/B: The Sensex was significantly cheaper compared to current levels only in the year after 9/11 and in the wake of the Lehman crash (exhibit 1).

P/B: The Sensex was significantly cheaper compared to current levels only in the year after 9/11 and in the wake of the Lehman crash (exhibit 1).

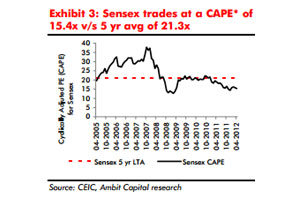

CAPE: On CAPE (i.e. cyclically adjusted real P/E), India has only once traded at lower multiples than the current 15x. This rare outcome materialized in the post-Lehman months when it hit 12x (see exhibit 3).

CAPE: On CAPE (i.e. cyclically adjusted real P/E), India has only once traded at lower multiples than the current 15x. This rare outcome materialized in the post-Lehman months when it hit 12x (see exhibit 3). Investment Implications: Buy Good & Clean stocks

Investment Implications: Buy Good & Clean stocks

Given that India appears oversold on long term metrics, unless you believe that there is another Lehman on the way, it makes sense to take a bolder approach to

buying high-quality, sensibly-valued companies in India. Fifty such companies were highlighted in our "Good & Clean 4.0: the Great 50" note published on May 03, 2012.

Furthermore, leaving our charts aside, it is worth considering the three upcoming catalysts highlighted in our email last week (India Strategy: Blinkered by all the

doom & gloom", May 16, 2012) in case your spirit is willing to buy India but the flesh is weak:

1. Change in FM: With the current FM likely headed for a more prestigious but more titular role, the three candidates who appear to be in the frame for the FM’s role appear to be more progressive candidates than the incumbent.

2. More QE from the West: We have seen the QE playbook being rolled out repeatedly by the ECB and the Fed. Given the potential risks to the European banking system and given a pro-growth (hence anti-austerity) leader heading France, it would be very strange if the ECB did not use the monetary fire hose to calm the markets down eventually.

3. Oil: India's oil import bill amounts to 7% of our GDP. Therefore, a 10% fall in the price of oil (from US$110/Brent barrel to US$100) will reduce our current

account deficit by 40bps. We are not oil experts but looking at the weakening Chinese economy and listening to the Saudis talk about how they will work proactively to push Brent to US$100, we cannot but feel optimistic.

(Saurabh Mukherjea is the head of Institutional Equities at Ambit Capital.)