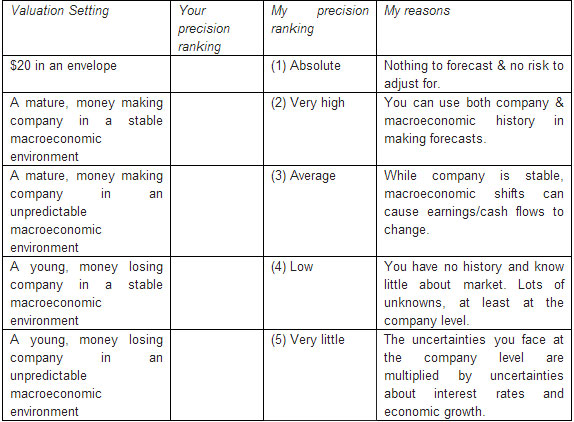

One of the responses to my last post on valuing young companies was that even if you can value companies early in the life cycle, you cannot do so with any degree of confidence. I concede that point, but that is exactly why I would try to value them! I know that statement makes little sense, but to solidify my argument, take a look at the following list of five assets/entities and rank them on the basis of the confidence you will feel in valuing each one (I have provided my rankings and the reasons in the table).

My guess is that your rankings will match closely to mine. Cash in an envelope is easier to value than an ongoing business, an ongoing stable business is easier to value than a young, growing business and valuations in general are easier when interest rates and economic growth are stable/predictable than when they are not.

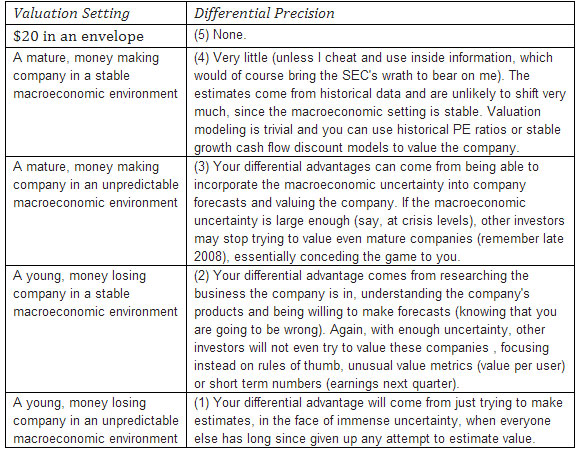

Now that we have dispensed with that formality, I think it is worth asking a more complex question. If valuation is designed to find investment bargains, what is the payoff to doing valuation in each of these settings? Note that the game is now different, since your advantage does not come from the precision of your valuation but in its relative precision: How much more precise is your estimate of value for a given asset is than the estimates of others valuing exactly the same asset? Here is my attempt to look at my potential differential advantages (and I would encourage you to do the same).

My motto is that you don’t have to be right to make money, but just less wrong than everyone else in the market. That makes my odds best in exactly those environments where I am uncomfortable and uncertainty is overwhelming.

Wielding Ben Graham’s tome on security analysis as a weapon, old-time value investors will probably take issue with this argument, pointing to the efficacy of the time-tested value investing conventions, where you are told to stay focused on companies with solid earnings and cash flows, with superior management. I would be inclined to concede the argument, if active value investing, as practiced today, actually worked, but there is little evidence that it does, at least in the aggregate, as I argued in this paper. In fact, there is evidence, albeit weak, that the average active growth investor beats a growth index more frequently and by more than the average active value investors beats a value index. That does not surprise me in the least, since it is in keeping with my thesis that the best investment opportunities are in the volatile, growth sectors.

I think that Ben Graham, if he were writing his book today, would be much less rigid in his view of value than the classicists. The real lesson that I get from reading Graham’s writings is that value is determined by fundamentals and that markets sometimes misread or ignore those fundamentals. My addendum is that investors are more likely to misread and/or ignore fundamentals, when they are faced with large uncertainties than with small ones.

In closing, there are three general propositions about valuation that flow from my view of uncertainty.

1) The more comfortable you are in valuing a company, the less point there is to doing that valuation. After all, the factors that comfort you are just as likely to comfort others valuing that company.

2) If you wait for the uncertainties to resolve themselves before you value a company, it is too late for a valuation. In the midst of crises or uncertainty, it is human nature to want to wait, until there is resolution, before committing to valuation or investing. It is precisely at the moment of crisis, though, that your valuation skill set will provide the biggest payoff, if employed. So, you should have been valuing banks in November 2008, Greek companies in 2009 and 2010 and emerging market companies earlier this year. Using a specific example, many global investors are holding back on investing in India, waiting for the election that is scheduled next year, making me more interested in valuing Indian companies today, and especially those that are more likely to be affected by the election results.

3) If most investors contend that something cannot be valued, you should try to value it. As I noted in my last post, I think that the status quo (where young companies are not valued) suits both investors and traders, the former, because they can stay above the fray, attributing any profits to be made in in these companies to gambling, and the latter, because they feel no obligation to even pay lip service to fundamentals.

If you have found conventional valuation to be an extension of accounting and therefore boring (I am sorry! My biases are showing!), you should try valuing young, growth companies instead, to see how much fun it can be to connect stories to numbers and narratives to value. So, rather than value 3M or Coca Cola for the hundredth time, why not try valuing Tesla, Yelp or Pandora? And if in the process, you make some money, that is just icing on the cake, right?

(Aswath Damodaran is a professor of finance at the Stern School of Business at NYU.)

To become a guest contributor with VCCircle, write to shrija@vccircle.com.