Investors, analysts and financial journalists use different measures of value to make their investment cases and it is not a surprise that these different value measures sometimes lead to confusion. For instance, at the peak of Apple's glory early last year, there were several articles making the point that Apple had become the most valuable company in history, using the market capitalization of the company to back the assertion. A few days ago, in a reflection of Apple's fall from grace, an article in WSJ noted that Google had exceeded Apple's value, using enterprise value as the measure of value. What are these different measures of value for the same firm? Why do they differ and what do they measure? Which one is the best measure of value?

What are the different measures of value?

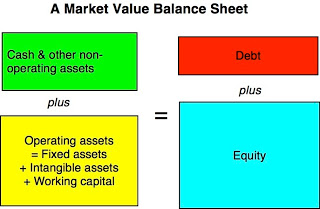

To see the distinction between different measures of value, I find it useful to go back to a balance sheet format, with market values replacing accounting book values. Thus, the market value balance sheet of a company looks as follows:

Note that operating assets include not only fixed assets, but also any intangible assets (brand name, customer loyalty, patents etc.) as well as the net working capital needed to operate those assets and that debt is inclusive of all non-equity claims (including preferred equity).

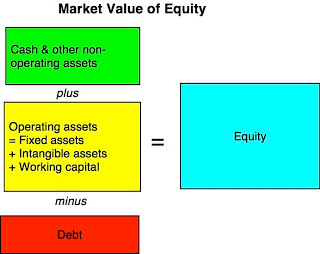

Let's start with the market value of equity. Rearranging the financial balance sheet, the market value of equity measures the difference between the market value of all assets and the market value of debt.

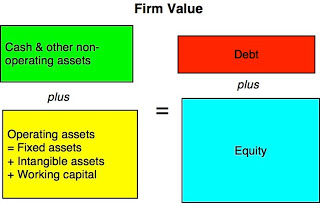

The second measure of market value is firm value, the sum of the market value of equity and the market value of debt. Using the balance sheet format again, the market value of the firm measures the market's assessment of the values of all assets.

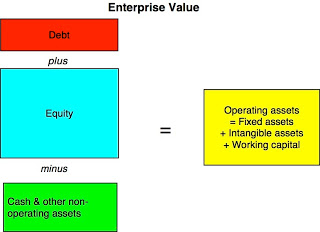

The third measure of market value nets out the market value of cash & other non-operating assets from firm value to arrive at enterprise value. With the balance sheet format, you can see that enterprise value should be equal to the market value of the operating assets of the company.

One of the features of enterprise value is that it is relatively immune (though not completely so) from purely financial transactions. A stock buyback funded with debt, a dividend paid for from an existing cash balance or a debt repayment from cash should leave enterprise value unchanged, unless the resulting shift in capital structure changes the cost of capital for operating assets, which, in turn, can change the estimated value of these assets.

The measurement questions

To arrive at the market values of equity, firm and enterprise, you need updated "market" values for equity, debt and cash/non-operating assets. In practice, the only number that you can get on an updated (and current) basis for most companies is the market price of the traded shares. To get from that price to composite market values often requires assumptions and approximations, which sometimes are merited but can sometimes lead to systematic errors in value estimates.

I. Market value of equity

While the conventional practice is to multiply the shares outstanding in the company by the share price to get to a market capitalization and to use this market capitalization as the market value of equity, there are three potential measurement issues that have to be confronted:

1. Non-traded shares: There are some publicly traded companies with multiple classes of shares, with one or more of these classes being non-traded. Though these non-traded shares are often aggregated with the traded shares to arrive at share count and market cap, the differences in voting rights and dividend payout across share classes can make this a dangerous assumption. If you assume that the non-traded share have higher voting rights, it is likely to you will understate the market value of equity by assigning the share price of the traded shares to them.

2. Management options: The market value of equity should include all equity claims on the company, not just its common shares. When there are management options outstanding, they have value, even if they are not traded, and that value should be added to the market capitalization of the traded shares to arrive at the market value of equity in the company. For a company like Cisco, this can make a significant difference in the estimated market value of equity (and in the ratios like PE that are computed based on that market value). Again, using short cuts (such as multiply the fully diluted number of shares by the share price to get to market capitalization) will give you shoddy estimates of market value of equity.

3. Convertible securities: To the extent that a company raised funds from the use of bonds or preferred stock that are convertible into common equity, the conversion option should technically be treated as part of the value of equity (and not as debt or preferred stock). Failing to do so will understate the market value of equity in companies with lots of convertible securities outstanding.

II. Debt

In theory, the firm and enterprise values of a company should reflect the market value of all debt claims on the company. In practice, this is almost never the case for two reasons:

1. Non-traded debt: The problem of non-trading is far greater with debt than equity, because bank debt is a large proportion of overall debt, even for many companies that issue bonds, and is the only source of debt for companies that don't issue bonds. Lacking a market value, many analysts have resorted to using book value of debt in their firm value and enterprise value computations. Though the effect of doing so is relatively small for healthy companies (book values of debt are close to market values of debt), it can be large for distressed companies, where the book value of debt will be far higher than the market value of that debt, leading to much higher estimates of enterprise and firm value for these firms than is merited.

2. Off balance sheet debt: To the extent that firms use off-balance sheet debt, we will understate the firm and enterprise values for these firms. While this may sound like a problem only with esoteric firms that play financing games, it is actually far more prevalent, if you recognize lease commitments as debt. Most retailers and restaurant companies have substantial lease commitments that should be converted into debt for purposes of computing firm or enterprise value.

III. Cash

Cash should be simple to value, right? That is generally true but even with cash there are questions that analysts have to answer:

1. Operating versus non-operating cash: To the extent that some or a large portion of the cash balance that you see at a company may be needed for its ongoing operations, you should be separating this portion of the cash from the overall cash balance and bringing into the operating asset column (under working capital). There are two problems we face in making this distinction between operating and excess cash. The first is that operating cash needs will be different across different businesses, with some businesses requiring little or no operating cash and others requiring more. The second is that cash needs have changed over time, with a shift away from cash based transactions in many markets and companies collectively require less cash than they used to a few decades ago. Analysts and investors, for the most part, have no stomach for making the distinction between operating and non-operating cash on a company-by-company basis and use one of two approximations. The first is to assume no operating cash and treat the entire cash balance as excess cash in computing enterprise value. The second is to use a rule of thumb to compute operating cash, such as setting cash at 2% of revenues for all firms. Again, while either approach may do little damage to value estimates at the typical firm, they will both fail at exceptional firms, where the cash balances are very large (as a proportion of value) but are untouchable because they are is needed for operations.

2. Trapped cash: In the last decade, US companies with global operations have accumulated cash balances from their foreign operations that are trapped, because using the cash for investments in the US or for dividends/buybacks will trigger tax liabilities. If a company has a very large cash balance and a significant portion of that cash is trapped, it is possible that the market attaches a discount to the stated value to reflect future tax payments. Netting out the entire cash balance to get to enterprise value will therefore give you too low an estimate of enterprise value, a point to ponder when netting out the $145 billion (with >$100 billion trapped) in cash to get to Apple's enterprise value.

IV. Other non-operating assets

When companies have non-cash assets that are non-operating, your problems start to multiply. With many family group companies, where cross holdings are the rule rather than the exception, the effect of miscalculating the value of non-operating assets can be dramatic.

1. Cross holdings in other companies: When a company has non-controlling stakes in other companies, the market value of these holdings should be netted out to get to the enterprise value of the parent company. Doing so may be straightforward if the cross holdings are in other publicly traded companies, where market prices are available, but it will be difficult if it is in a private business. In the latter case, the value of the cross holding on the balance sheet will, in most cases, reflect the book value of the investment, with little information provided to estimate market value. The problems become worse if there are dozens of cross holdings, rather than just a handful. Not surprisingly, most analysts completely ignore cross holdings in computing enterprise value and the remaining net out the book value of the holdings. For companies that derive a large proportion of their value from cross holdings, this will lead to an upwardly biased estimate of enterprise value. When a company has a controlling or a majority stake in another company, a different kind of problem is created when computing enterprise value. The market value of equity in the parent company reflects only the majority stake in the subsidiary but the debt and cash in the computation are usually obtained from consolidated balance sheets, which reflect 100% of the subsidiary. To counter this inconsistency, analysts add the minority interest (which is the accountant's estimate of the equity in the non-owned portion of the subsidiary) to arrive at enterprise value, but the minority interest is a book value measure.

2. Double counting of operating assets: One of the real dangers of fair value accounting and its push to bring more invisible or intangible assets to the balance sheet is that it increases the risk that analysts will double count. Thus, even if brand name and customer lists are valued and put on the balance sheet, they are very much part of the operations of the firm and should not be netted out as non-operating assets. Only assets that don't contribute (and are never expected to contribute) to operating income can be treated as non-operating assets.

Mismatches and Measurement Errors

Looking at the standard practices in value estimation, there are two clear inconsistency problems that you see crop up. One is in the mixing of market values, estimated values and book values for different items in the computation. The other and related question is that the market values can be updated constantly but the book value based numbers are as of the last financial statement.

I. Market versus Book value

In a typical enterprise value computation, the only number that comes from the market is the market capitalization, reflecting the market value of equity in common shares. The remaining numbers all come from accounting statements and reflect accounting estimates of value, with varying implications. With debt, as we noted, the difference between book and market value is likely to be small for healthy firms but much larger for distressed companies. With cash, the accounting estimates of value should be close, with the caveat that trapped cash may be discounted by the market to reflect expected tax liabilities. With cross holdings, the gap between book and market value can vary depending on how old the holding is (with older holdings have larger gaps) and the accounting for that holding.

While getting true market values for bank debt and cross holdings may be a pipe dream, there is no reason why we cannot estimate the market values for both. For debt, this will require using the interest expenses and average maturity on the debt to compute an estimated market value of the debt (akin to pricing a coupon bond). With cross holdings (minority holdings and interests), it may require us to use sector average price to book ratios to estimate the values of the cross holdings.

II. Timing Differences

While you would like values to be current (since your investment decisions have to reflect current numbers), only market-based numbers can be updated on a continuous basis. The only market-based number in most enterprise value calculations is the market capitalization number (reflecting current stock prices), with the other numbers either directly coming out of accounting statements (debt, cash) or indirectly dependent on information in them (options outstanding, lease commitments). There are two questions, therefore, that you have to confront: (a) Should you try for timing consistency or current value? (b) If you go current value, what types of biases/problems will you face because of the timing mismatch?

1. Consistency versus Current Values: If you are using the value estimates to look at how values change over time or why values have varied across companies in the past, consistency may win over updating. Thus, rather than using the current market value of equity, you may use the market value of equity as of date of the last financial statement. If you using the value estimates to make investment or transaction judgments today, the current value rule should win out. After all, if you find a company to be cheap, you get to buy it at today's price (and not the price as of the last financial statement).

2. Biases/Errors from Time mismatches: Assuming that the need to be updated wins out, your biggest concern with using dated estimates of debt, cash and other non-operating assets is that their values may have shifted significantly since the last reporting date. Not only can companies borrow new debt or repay old debt, which can affect the cash balance, but the operating needs of the company can lead to a decline or augmentation in the cash. For young growth companies, with large investment needs and/or operating losses, the cash balance today can be much lower than it was in the last financial statement. For mature companies in cashflow-rich businesses, cash balances can be much higher than in the last financial statement.

In fact, the mismatch can sometimes lead to strange results, especially for young, growth companies that have had operating/financial/legal problems in the very recent past. A drop in market capitalization combined with a cash balance from a recent financial statement that is much higher than the true cash balance can combine to create negative enterprise values for some firms.

Financial service companies

This discussion has been premised on two assumptions, that debt is a source of capital and that cash is a non-operating asset to businesses. There is a subset of the market where both assumptions break down and it is especially so with financial service companies, where debt is more raw material than source of capital and cash & marketable securities cannot be claimed by investors. With banks, investment banks and insurance companies, the only estimate of value that should carry weight is the market value of equity. You can compute the enterprise values for JP Morgan Chase and Citigroup but it will be an academic exercise that will yield absurdly high numbers but will provide little information to investors.

The Numbers

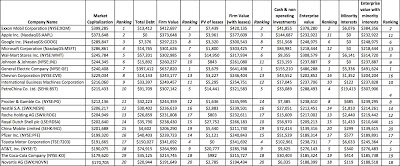

To illustrate the difference between the different measures of value, I first screened for global non-financial service companies with market capitalizations exceeding $25 billion and computed the firm and enterprise values for each of them. You can download the entire spreadsheet of 292 companies by clicking here. I then created a list of the top 20 companies by market capitalization and ranked them based upon the other measures of value as well.

Apple is more valuable than Google, if you use market capitalization as your measure of value, whereas Google is more valuable than Apple, if you use enterprise value, and GE dwarfs both companies, based upon enterprise value, because it has $415 billion in debt outstanding. Note that much of this debt is held by GE Capital and given my earlier point about debt, cash and enterprise value being meaningless in a financial service company, I would view GE's enterprise value with skepticism. Nothing in this table tells me which companies are good investments and which ones are over priced and all the caveats about mixing market and book value, timing differences and missing numbers apply.

Why have different measures of value?

Having multiple measures of value can create confusion, but there are two good reasons why you may see different measures of value and one bad one.

1. Transactional considerations

The measure of value that you use can vary, depending on what you are planning to acquire as an investment. For instance, in acquisitions, where the acquiring firm is planning on acquiring the operating assets of the target firm, it is enterprise value that matters, since the acquiring firm will use its own mix of debt and equity to fund the acquisition and will not lay claim on the target company's cash. In contrast, if you are an individual investor in a publicly traded company, the market capitalization may be your best measure of value since you have little control over how much debt the company has or how much cash it holds. In fact, enterprise value based calculations can be misleading for individual investors, since they can mask default risk: a firm on the verge of default can look cheap on an EV basis.

2. Consistency in multiples

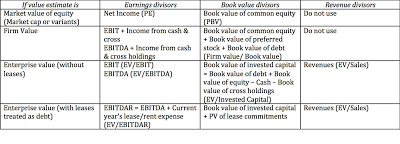

In investing, we use estimates of market value to arrive at measures of relative value (multiples), so that we can compare how the market is pricing comparable companies. Relative value requires that the market value be scaled to a common variable (earnings, revenues, book value) and is governed by a simple consistency rule. The measure of value that we use in the numerator of a multiple should be consistent with the measure of earnings or book value that we use in the denominator. Equity values should be matched up to equity earnings or book equity and enterprise values to operating income or book capital. Consider, for instance, PE ratios and EV/EBITDA multiples. The PE ratio is obtained by dividing the market value of equity by the net income (or price per share by earnings per share); both the numerator and denominator are equity values. The EV/EBITDA is obtained by dividing the enterprise value (market value of operating assets) by the EBITDA (the cash flow generated by these operating assets). In the table below, I list the potential choices when it comes to consistent multiples:

3. Agenda-based value estimation

In some cases, the choice of value measure may depend upon the agenda or biases of the analyst in question. Thus, an analyst that is bullish on Apple will latch on to its enterprise value to make his or her case, since it makes Apple look much cheaper.

Closing thoughts

When it comes to which value estimate is the best, I am an agnostic and I think each one carries information to investors. The PE ratio may be old fashioned but it still is a useful measure of value for individual investors in companies, and enterprise value has its appeal in other contexts. Understanding what each value measure is capturing and being consistent in how it is computed, compared and scaled is far more important than finding the one best measure of value.

(Aswath Damodaran is a professor of finance at the Stern School of Business at NYU.)

To become a guest contributor with VCCircle, write to shrija@vccircle.com.