Indian capital market regulator SEBI has unveiled the final norms to regulate all alternate investment funds active in the country, including private equity, venture capital funds and hedge funds, toning down certain conditions it had earlier proposed while simplifying the categories under which the funds will be bracketed.

The key changes (also see the graphic highlights) from the draft regulations proposed last year (more on that here) relate to the cut in GP/sponsor contribution from 5 per cent of the total corpus to 2.5 per cent or Rs 5 crore ($1 million), whichever is lower. This would make it easier for fund managers to float new funds, especially large funds.

Most large funds today are raising around $500 million and the new norms would mean fund managers or sponsors would need to bring in just $1 million as against 5 per cent of the corpus or $25 million that they would have required to bring in as per the draft proposal.

Another big change has come in terms of making it simpler for funds to classify themselves instead of putting them under strict category baskets. The draft norms had called for all funds to be classified under nine categories, which left a big question mark on the future of private equity investment in bulk of Indian firms listed on the stock exchanges besides the operational leeway for funds which have sector-agnostic investment strategy.

The revised norms have put all funds under three categories to be governed separately in terms of tax incentives, investment horizon and other norms.

Somasekhar Sundaresan, partner at the law firm J Sagar Associates, said, “It is apparent that what SEBI’s board members have approved today is substantially different from the concept note that came out last year. This is a welcome development since the concept note intended to micro-manage the specific asset classes into which a fund could invest.”

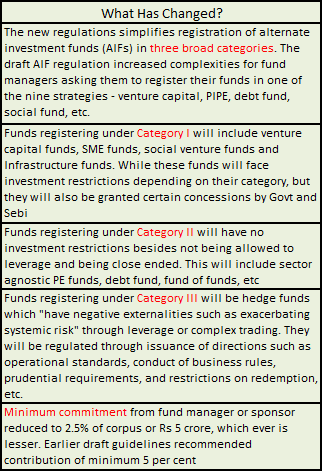

AIF I, the first category includes those with ‘positive spill-over effects on the economy’. SEBI is looking at giving certain incentives or concessions from government and other regulators as well. Funds that qualify under this category include venture capital funds, small and medium enterprises (SME) funds, social venture funds and infrastructure funds. SEBI has said that these funds will be close ended and they cannot engage in leveraging.

In the second category or AIF II, SEBI has included funds which can undertake leverage only to meet their day-to-day operational requirements. This category includes private equity funds, debt funds, fund of funds and such other funds that are not classified as category I or III, SEBI said. These funds too will be close ended as per the regulations but will have no other investment restrictions.

Under AIF III, SEBI has included hedge funds which are considered to have ‘negative external externalities such as exacerbating systemic risk through leverage or complex trading strategies’. SEBI has clearly mandated that this category shall be governed by the board and these funds can either be open ended or close ended, also it may engage in leveraging subject to limits specified by the board.

Other key areas where SEBI has put its foot down include not allowing any AIF to accept any investment below Rs 1 crore from an investor (which would mean keeping small investors out of the ambit of such riskier asset classes) and the AIF shall have a minimum corpus of Rs 20 crore. It has also specified that none of the funds can have more than 1,000 investors in each AIF.

According to sources in the know, the private equity industry had made its representation to SEBI and had requested to keep the minimum to be raised from an individual at Rs 50 lakh to pool in funds from more HNIs and individual investors. In the end Sebi went ahead with a higher floor for such individual investments.

The market regulator has also mandated that AIFs will not be permitted to invest more than 25 per cent of the investible funds in one company. Further they cannot invest in associate companies.

SEBI has also said units of AIF may be listed on stock exchange subject to a minimum tradable lot of Rs 1 crore but in any given point they cannot raise money through public listing mechanism.

Sundaresan of JSA added, “The product-design-based classification appears to have been abandoned, with the focus now being on systemic risk and investor protection. One would have to wait for the final fine-print to be notified, which is expected in about a month.”

The norms mean all AIFs whether operating as PE funds, real estate funds, hedge funds, etc. must register with SEBI under the AIF Regulations. While the existing SEBI (Venture Capital Funds) Regulations, 1996 shall be repealed, existing VCFs shall continue to be regulated by the VCF Regulations till the existing fund or scheme managed by the fund is wound up.

Existing VCFs, however, shall not raise any fresh funds after the final regulations are notified except commitments already made by investors as on date of the notification. Such VCFs may also seek re-registration under AIF regulations subject to approval of two thirds of their investors by value.

Existing funds not registered under the VCF Regulations will not be allowed to float any new scheme without registration under AIF Regulations. However, schemes floated by such funds before coming into force of AIF Regulations, shall be allowed to continue to be governed till maturity by the contractual terms, except that no rollover/ extension or raising of any fresh funds shall be allowed.

Existing funds not registered under the VCF Regulations which seek registration but are not able to comply with all provisions of AIF Regulations may seek exemption from SEBI from strict compliance with the AIF Regulations.

Gopal Srinivasan, MD of TVS Capital, says, “The fact that SEBI has come out with classification in three simple buckets indicates that it has taken the recommendations made by various organisations and individuals. The regulations also show that Rupee capital pools will now get much more attention, especially the funds of funds, which will allow HNIs to participate in the market through sophisticated vehicles. The norms for hedge funds will bring more attention to capital markets and lead to higher efficiency in the system.”

See Our Previous Report:

Alternate Investment Funds To Come Under SEBI Lens