Raghuram Rajan, India’s outspoken central bank governor, will quit office on Saturday to make way for his deputy, the reticent Urjit Patel.

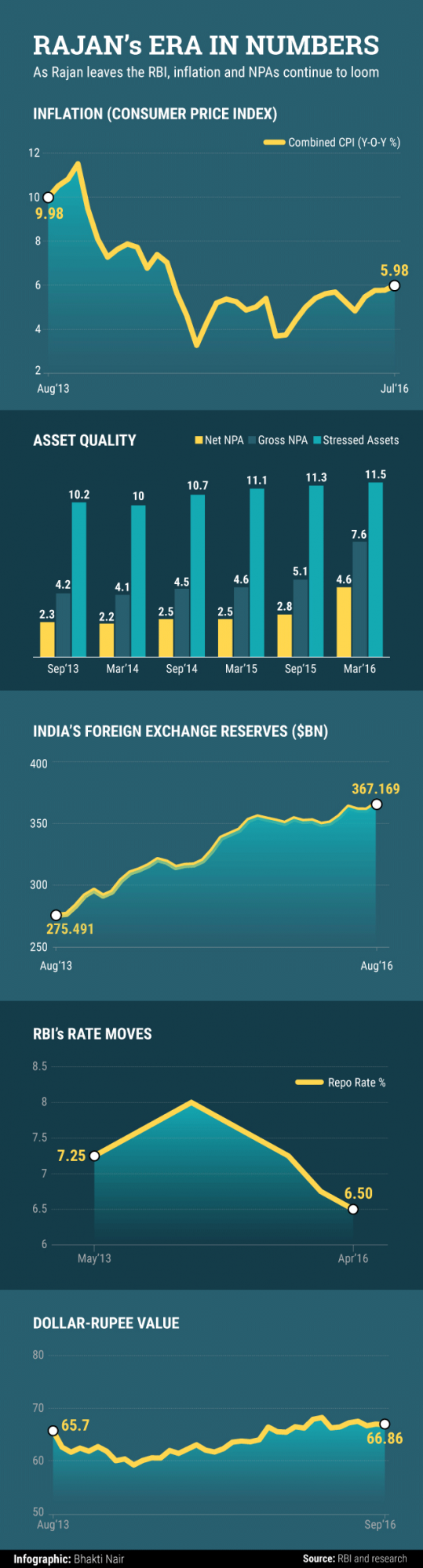

Rajan’s tenure at the Reserve Bank of India (RBI) will be remembered best for his crusade against inflation. But as he leaves office, inflation remains perilously close to the government’s upper tolerance limit of 6% and well above its five-year target of 4%.

The former International Monetary Fund chief economist also pushed banks to reveal the full extent of bad loans on their books and take measures to contain the problem.

When Rajan took office, the repo rate—the RBI’s main lending rate—was at 7.25%. The rate touched 8% in his first three months at the RBI. But since January 2015 he has brought down the repo rate to 6.5%, the lowest since March 2011.

Corporate India wanted him to go lower still, but he did not oblige. Eventually, this would turn out to be his proverbial Achilles heel.

Rajan’s utterances outside of his brief often made more news than those on the central bank’s monetary policy. His critical comments on the Narendra Modi regime’s flagship ‘Make in India’ initiative and on the issue of tolerance certainly didn’t go down well with sections within the government, the ruling Bharatiya Janata Party and its parent the Rashtriya Swayamsevak Sangh.

This friction, perceived or real, eventually led to allegations, prompting him not to seek a second term. Several analysts feel that Patel’s relative reticence could mean he will have smoother relations with the government.

On the flip side, it will also mean that the markets will find it much harder to second guess Patel’s moves, especially when the newly constituted Monetary Policy Committee, in which he has a casting vote, begins deciding on policy rates.

Like this report? Sign up for our daily newsletter to get our top reports.