\n

Over the last several years, the IPO market in the United States has practically disappeared. Just 12 companies went public in the United States in the first half of 2009, and only eight of them were U.S. companies. Is the U.S. IPO market going through a cyclical downturn exacerbated by the recent credit crisis, or is today’s market structure failing the IPO?

\n

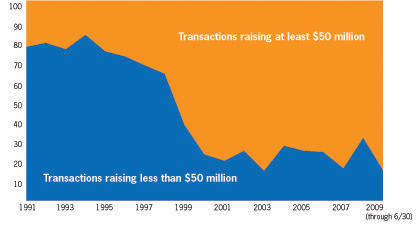

From 1991 to 1997 nearly 80% of the IPOs were smaller than $50 million. By 2000 the number of sub-$50 million IPOs had declined to only 20% of the market. The market for underwritten IPOs, given its current structure, is closed to 80% of the companies that need it.

\n

Market structure is causing the IPO crisis explores lessons learned, the IPO crisis, and Grant Thornton LLP’s ideas for an issuer and investor opt-in capital market structure that is conducive to capital formation and favors small, mid and large cap companies.

\n

\n

Conclusion

\n

Alternative Public Market Segment

\n

The United States needs an issuer and investor opt-in capital market that provides the same structure that served the United States in good stead for so many years. This market would make

use of full SEC oversight and disclosure, and could be run as a separate segment of NYSE or NASDAQ, or as a new market entrant. It would be:

\n

• Opt-in/Freedom of Choice – Issuers would have the freedom to choose whether to list in the alternative marketplace or in the traditional marketplace. Issuers could choose to move from their current market segment into the alternative market segment (we suspect that many small companies would make this selection, while large cap companies would not). Investors would have the freedom to buy and sell stocks from either market. This is a “let-thebest-

solution-win” approach that will re-grow the ecosystem to support small cap stocks and IPOs.

\n

Public – Unlike the 144A market, this market would be open to all investors. Thus, brokerage accounts and equity research could be processed to keep costs under control and

to leverage currently available infrastructure.

\n

• Regulated – The market would be subject to the same SEC corporate disclosure, oversight and enforcement as existing markets. However, market rules would be tailored

to preserve the economics necessary to support quality research, liquidity (capital commitment) and sales support, thus favoring investors over high-frequency and day trading.

Traditional public (SEC) reporting and oversight would be in place, including Sarbanes-Oxley.

\n

Quote driven – The market would be a telephone market supported by market makers or specialists, much like themarkets of a decade ago. These individuals would commit

capital and could not be disintermediated by electronic communication networks (ECNs), which could not interact with the book.

\n

• Minimum quote increments (spreads) at 10 cents and 20 cents and minimum commissions – 10 cent increments (spreads) for stocks under $5.00 per share, and 20 cent increments for stocks $5.00 per share and greater, as opposed to today’s penny spread market. The increments

could be reviewed annually by the market and the SEC. These measures would bring sales support back to stocks and provide economics to support equity research independent of investment banking.

\n

• Broker intermediated – Investors could not execute direct electronic trades in this market; buying stock would require a call or electronic indication to a brokerage firm. Brokers once

again would earn commissions and be incented to phone and present stocks to potential investors. These measures would discourage day trading.

\n

Research requirement – Firms making markets in these securities would be required to provide equity research coverage that meets minimum standards, such as a thorough initial report, quarterly reports (typically a minimum of 1-2 pages) and forecasts.

This structure would lead to investment in the types of investment banks that once supported the IPO market in this country (e.g., Alex. Brown & Sons, Hambrecht & Quist, L.F.

Rothschild & Company, Montgomery Securities, Robertson Stephens) and would trigger rejuvenated investment activity and innovation.